Global markets lost momentum into Thursday’s session as renewed US-Iran tensions, rising oil prices and another push higher in bond yields unsettled investors ahead of crucial US inflation data.

While the AI-driven equity rally continues to provide substantial support for risk assets, traders are becoming increasingly uneasy that persistent energy inflation and tighter financial conditions may eventually begin colliding with stretched equity valuations.

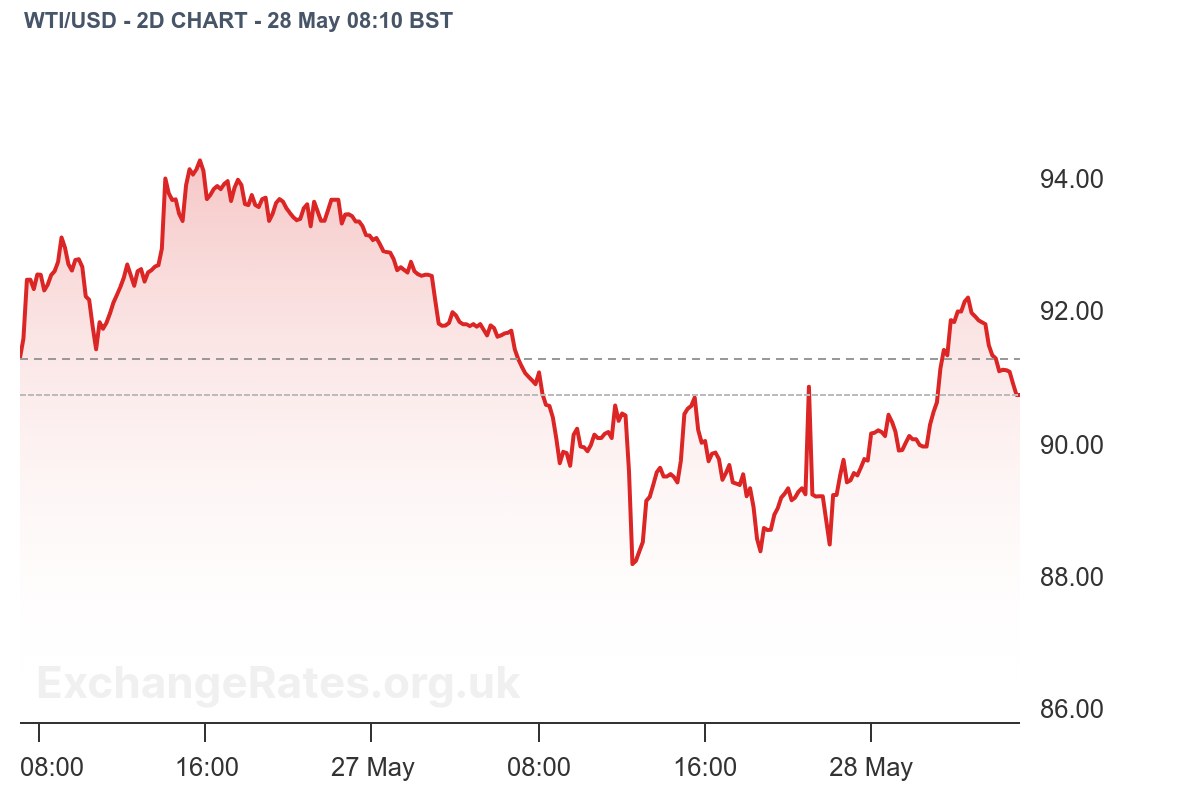

The tone across global markets deteriorated notably overnight after fresh military developments in the Gulf reignited concerns that the recent optimism surrounding a possible US-Iran agreement may have been premature.

Reports of renewed US defensive strikes against Iranian drones, alongside warning shots fired toward vessels attempting to leave the Strait of Hormuz, pushed crude prices sharply higher once again.

Brentfutures rebounded aggressively back toward the upper-$90 region after Wednesday’s heavy reversal lower, while Gulf shipping costs and insurance premia continue to climb.

More importantly for broader markets, investors are increasingly beginning to treat the conflict as something more persistent than a short-lived geopolitical shock.

That shift has become increasingly visible in bond markets, where yields continue grinding higher despite softer equity sentiment overnight.

The US 10-year Treasury yield moved back toward the 4.50% region, while traders continue reassessing how elevated oil prices and supply disruption risks could alter the Federal Reserve’s rate path later this year.

Lloyds Bank noted overnight that US manufacturers continue to display surprising resilience despite mounting input cost pressures.

Recent regional Fed surveys showed firms remaining broadly constructive on activity, employment and capital expenditure even as energy-driven price pressures squeeze margins.

According to Lloyds, businesses appear willing to look through the current Middle East disruption for now, although the bank warned that inflationary pressures may ultimately prove “more persistent than current expectations imply.”

That inflation narrative now sits firmly at the centre of today’s session, with markets turning their focus toward the US core PCE release — the Federal Reserve’s preferred inflation gauge.

SEB argued overnight that while some softer commodity components relative to CPI may modestly temper the PCE print, the broader concern is that the Fed’s patience with inflation is “running out,” particularly if energy costs continue feeding through into broader price expectations.

The bank also highlighted that markets are increasingly pricing the possibility of another Fed hike before year-end.

Underneath the AI-fuelled equity rally, though, rates are increasingly becoming the bigger problem.

Major US indices held up relatively well overnight, but there are clear signs investors are becoming more selective and increasingly sensitive to moves in bond yields.

Treasury markets have effectively become the dominant macro driver again, particularly as investors question whether higher energy costs and structurally elevated capital expenditure could keep inflation sticky well into 2027.

The AI trade nevertheless continues to absorb a remarkable amount of macro pressure.

Semiconductor stocks remain firmly at the centre of global equity flows, with investors still aggressively chasing AI-linked earnings momentum despite the deteriorating macro backdrop.

Nvidia’s blockbuster guidance continues reverberating through markets, while memory, cloud infrastructure and chip-design names remain heavily bid.

Reuters noted that overseas investors have now bought Japanese equities for eight consecutive weeks, with AI-linked technology names continuing to dominate inflows into Tokyo markets.

At the same time, rising Japanese yields are beginning to reshape broader global capital flow dynamics.

Japan Post Bank is reportedly considering doubling its domestic JGB holdings as part of a broader medium-term investment rethink. That development is drawing increasing attention given the critical role Japanese institutional investors play across global bond markets.

Single-stock moves were also aggressive overnight.

eToro highlighted growing speculation that the current equity rally could evolve into a broader “melt-up” scenario capable of pushing the S&P 500 toward the 8,000 level despite the ongoing bond market sell-off.

The Russell 2000’s breakout to fresh record highs has reinforced that idea, with smaller-cap and cyclical stocks increasingly joining the rally rather than the move remaining concentrated purely in mega-cap technology.

Travel and leisure stocks were among the strongest performers after earlier hopes of easing Middle East tensions briefly sent oil prices lower.

United Airlines rose 6%, Norwegian Cruise Line gained 6% and MGM Resorts surged 9% as traders priced in lower fuel costs and improving travel demand if geopolitical tensions eventually ease.

AI-linked earnings momentum also continued dominating after-hours flows. Snowflake surged more than 30% following a blowout quarter and a major expansion in AI infrastructure commitments, while Marvell rallied after significantly raising its long-term AI revenue outlook.

Dell remains one of Wall Street’s hottest momentum trades ahead of earnings later today after the stock more than doubled in just three months amid relentless enthusiasm surrounding AI server demand.

On the downside, Zscaler suffered its worst-ever trading session after weak guidance, management turnover and rising costs unnerved investors.

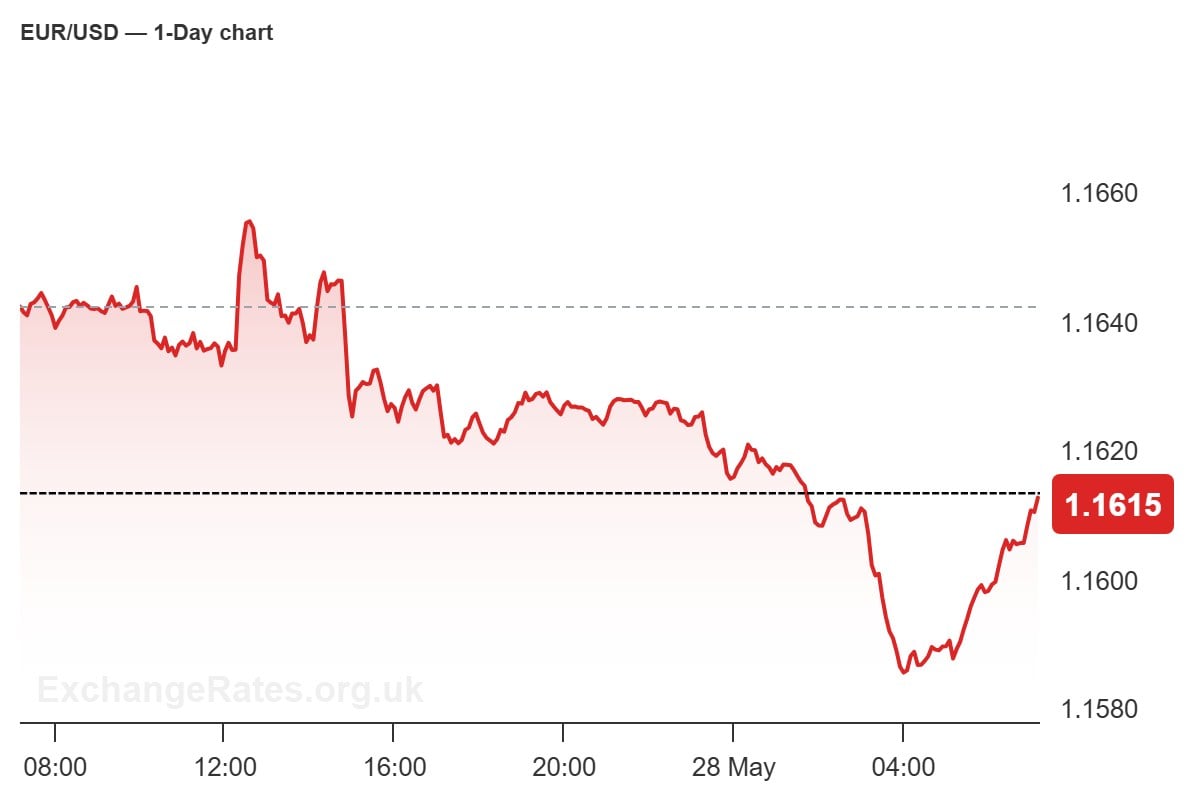

In FX markets, the US Dollar regained defensive support as geopolitical tensions intensified and Fed pricing remained tilted toward a more hawkish outlook.

ING described current trading conditions as a “headline-to-headline environment,” noting that renewed uncertainty surrounding US-Iran negotiations has restored much stronger macro support for the dollar compared with earlier in May.

EUR/USD briefly slipped below the 1.1600 level overnight as traders reacted to the worsening geopolitical backdrop. ING warned that the longer negotiations remain unresolved, the greater the inflationary impact on both the US and global economy, potentially limiting downside pressure on the dollar even if diplomacy eventually resumes.

The British Pound, meanwhile, has remained relatively stable, with foreign exchange analysts at ING suggesting much of the recent UK political risk premium has now faded from EUR/GBP pricing.

Commodity-linked currencies have struggled more noticeably.

The Australian and New Zealand dollars both weakened overnight as higher oil prices and softer Asian equities weighed on broader risk appetite.

Asian stock markets traded lower across the board, with South Korea and Japan particularly affected by rising Treasury yields and renewed Gulf tensions.

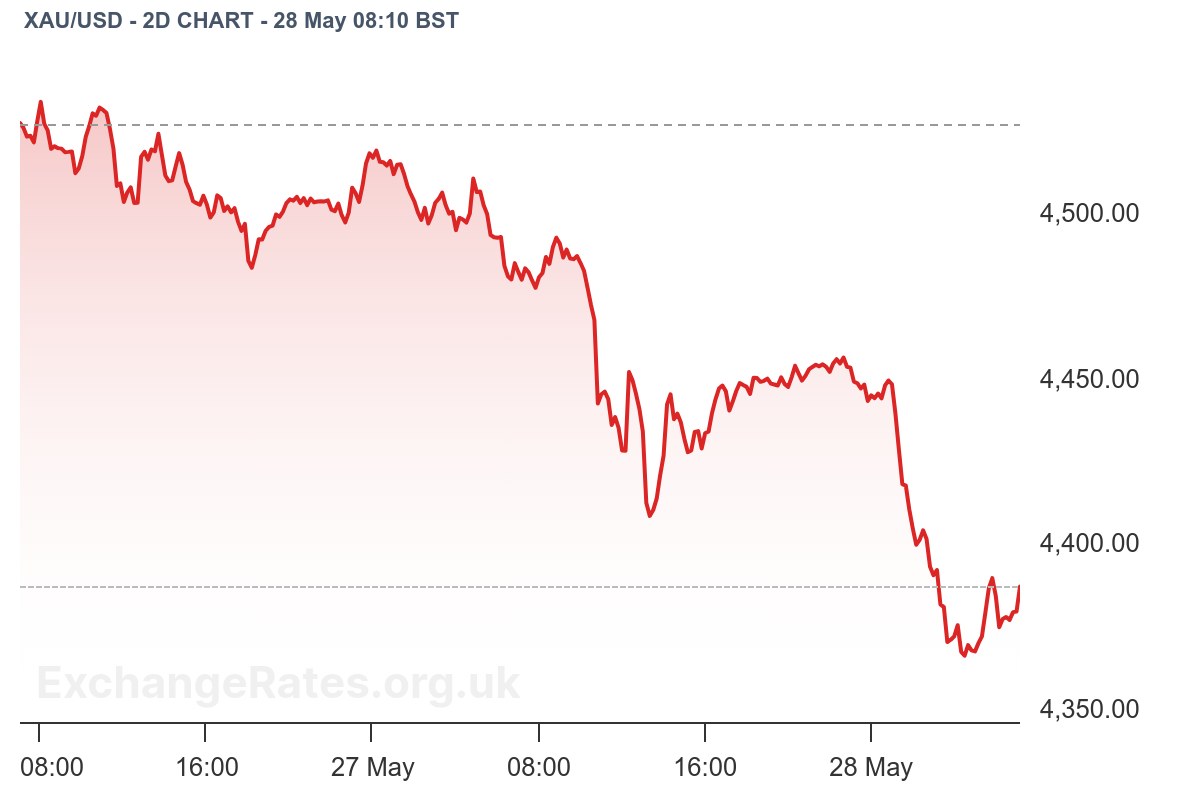

The price of Gold has also produced a surprisingly muted reaction.

Despite the deteriorating geopolitical backdrop, bullion has struggled to attract sustained safe-haven inflows, with rising real yields and a firmer dollar continuing to cap upside momentum.

Instead, traders appear far more willing to rotate toward cash and short-duration fixed income than aggressively chase gold higher.

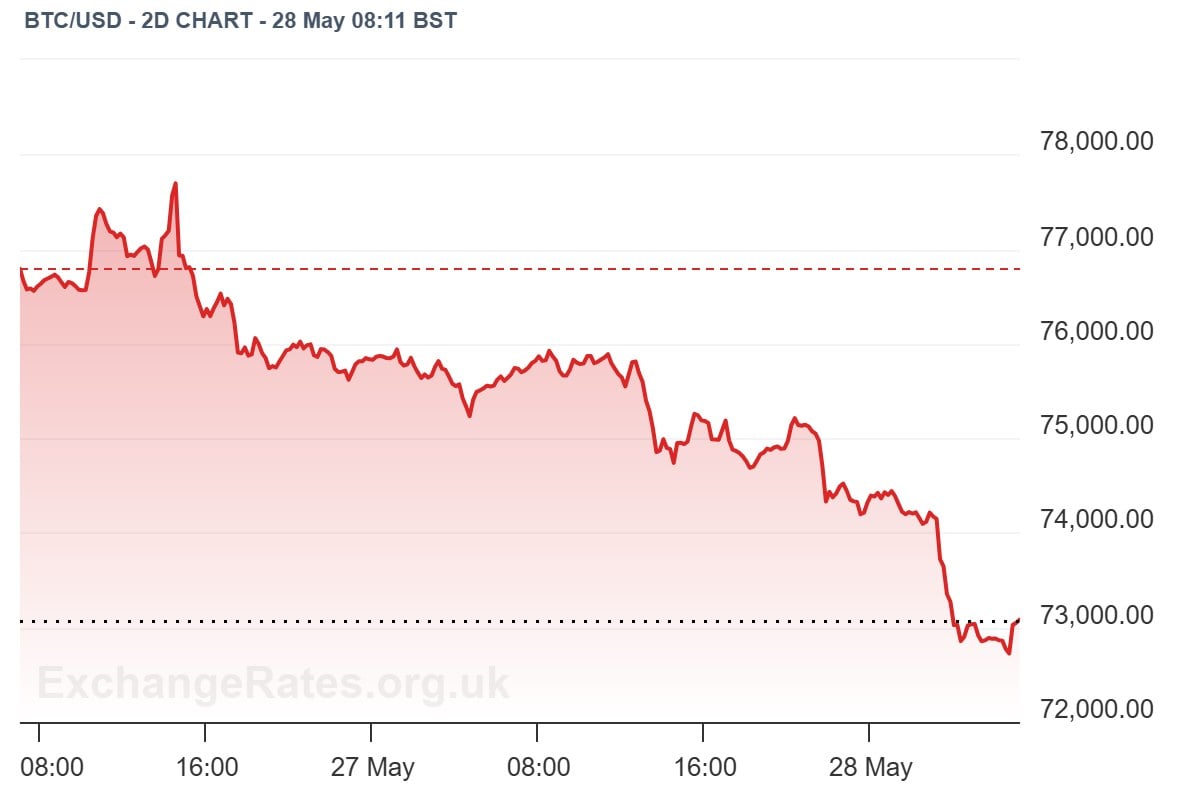

Crypto markets are also finding conditions increasingly difficult.

Bitcoin continues trading heavily amid tighter financial conditions, rising yields and softer speculative appetite, while ETF inflows have slowed materially from the pace seen earlier in the year.

Looking ahead, today’s macro calendar has the potential to generate significant cross-asset volatility, particularly given the increasingly fragile relationship between equities, bond yields and oil prices.

The main focus will be the US core PCE inflation release alongside GDP revisions, durable goods orders, personal income and spending, and weekly jobless claims.

Markets remain extremely sensitive to any upside inflation surprise following the recent rebound in energy prices and increasingly hawkish Fed pricing.

Traders will also monitor several Federal Reserve speakers through the session, including New York Fed President John Williams, while ECB President Lagarde and other ECB officials are also due to speak.

Lloyds noted in a brief this morning that next week’s payrolls release is still expected to show continued labour market resilience, with consensus forecasts remaining comfortably above the estimated breakeven pace needed to stabilise unemployment.

There is also increasing focus on whether the current equity rally is broadening into a more speculative melt-up phase.

eToro highlighted today that analysts are increasingly discussing scenarios where the S&P 500 could eventually push toward the 8,000 level despite the violent repricing underway across global bond markets.

The Russell 2000’s breakout to record highs has reinforced that narrative, with smaller-cap and cyclical names increasingly participating alongside AI leaders.

Today’s session will also bring heavy focus on earnings, including Dell, Best Buy, Kohl’s and several major Canadian banks.

Dell in particular remains one of the market’s key AI momentum trades ahead of results, while Snowflake and Marvell continue dominating discussion after strong AI-related earnings updates overnight.

Beyond the macro data, traders will continue closely monitoring developments surrounding the Strait of Hormuz and broader Gulf shipping flows.

The EIA crude inventory report later in the session may also become an additional volatility catalyst for both oil prices and inflation expectations.

For now, markets remain trapped between two powerful forces: relentless AI-driven optimism supporting equities, and rising energy-driven inflation risks steadily pushing global bond yields higher.

The key question for investors is whether the AI earnings cycle can continue offsetting tightening financial conditions if oil prices remain elevated and central banks are ultimately forced to stay more hawkish for longer.

Stock markets reeled on Friday as surging bond yields and renewed inflation…

Language: English | Français | Español | Deutsch | Português | Netherlands | GB

Leave a Reply