Shares of Micron Technology (MU +8.80%) have rocketed past $1,000, propelling the company into the elite trillion-dollar club. That meteoric rise reflects the seismic shift that artificial intelligence (AI) is imposing on the semiconductor landscape, where memory chips have shifted from boring commodity to mission-critical infrastructure.

While Micron's rally is still in full swing, smart investors are wondering where the stock could be headed next. The answer will hinge on the durability of AI-driven data center demand, how Micron's valuation stacks up against both the memory market's volatile past and today's AI chip leaders, and whether the market has already fully priced in the best-case scenario.

Image source: Micron Technology.

The biggest catalysts for Micron's explosive ascent are surging demand for high-bandwidth memory (HBM) and advanced DRAM solutions. AI training and inference workloads require enormous bandwidth and capacity that conventional memory solutions struggle to deliver efficiently.

HBM gets layered directly alongside GPU clusters in servers, enabling the low-latency data movement that is essential for large language models (LLMs) and other compute-intensive applications. Micron, Samsung, and SK Hynix are the largest manufacturers of HBM.

Micron's management has repeatedly emphasized the extraordinary tightness in HBM supply relative to demand. Not only is the company's entire 2026 production capacity sold out, but all indications point to DRAM shortages lingering past 2027 as AI capital expenditures continue to accelerate.

According to data compiled by TrendForce, the size of the global memory market is expected to reach $1.3 trillion in 2027 — up 44% from 2026. TrendForce estimates that DRAM revenue will rise 303% this year to $619 billion and expand to $903 billion in 2027.

As HBM and DRAM remain in short supply, producers like Micron should be able to sustain meaningful pricing power — supporting the case for robust gross margins that the memory market rarely sees.

The memory market has historically been notoriously cyclical. During past supercycles, Micron's price-to-earnings (P/E) multiple typically bottomed out between 3.5 and 8 as investors cautiously priced in the near-certainty that as the chipmakers rushed to expand their production capacity, they would inevitably overshoot as a group, leading to an eventual oversupply and subsequent margin erosion.

Micron's current P/E of 48 looks expensive relative to its historical thresholds. The company's profitability has surged so rapidly in recent quarters that its P/E ratio only partially reflects a dramatically higher earnings per share (EPS) base rather than simple multiple expansion on static profits.

What differentiates the current environment from past cycles is Micron's ability to win longer-term customer commitments. The company has moved beyond spot-market negotiations and is securing multiyear supply agreements with hyperscalers that lock in both volume and pricing. These contracts should alleviate some of the boom-bust volatility that has historically plagued the memory market.

Against this backdrop, Micron's trailing P/E multiple of 48 captures both the immediate earnings inflection and the market's ongoing reassessment of memory's role as a durable component of AI infrastructure build-outs rather than as a pure commodity.

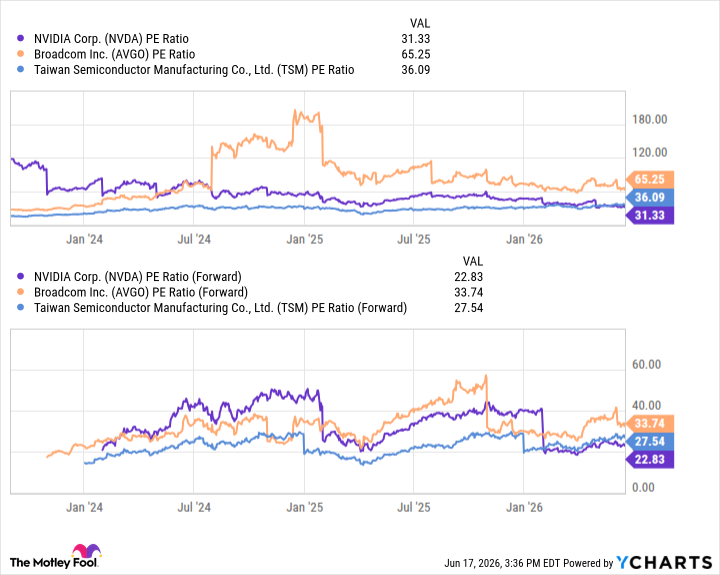

Comparing Micron to other prominent AI chip stocks can provide some useful context. Nvidia, Broadcom, and Taiwan Semiconductor Manufacturing are all leaders in their respective verticals within the chip value chain. Each stock has traded at elevated valuation multiples throughout the AI revolution — frequently carrying P/E multiples above 40.

NVDA PE Ratio data by YCharts.

The forward P/E multiples for each of these leaders have generally settled in the mid-20s to mid-30s range, even after meaningful stock price appreciation. These trends suggest investors remain confident in the multiyear visibility and pricing power that come with accelerating hyperscaler spending.

While Micron's trailing P/E multiple sits within or modestly below the peer range shown, its forward P/E of 9.5 is considerably more attractive, given the scale of its expected revenue and earnings growth over the next two or three years. This gap suggests Micron stock has further room for valuation expansion as the market rerates the stock in light of the structural shift in the nature of the company's business.

That said, investing in Micron stock is not without risk for investors. Should new foundry capacity from Micron and its competitors come online faster than investors anticipate, or if hyperscalers moderate their data center capital expenditures, its profit margins and valuation multiples will likely compress toward their historical averages.

Nevertheless, the combination of sold-out near-term HBM supply, multiyear contract visibility, and a modest valuation profile relative to other AI chip leaders suggests that Micron stock has room for meaningful upside before it reaches levels that would qualify it as fully priced for perfection.

Adam Spatacco has positions in Nvidia. The Motley Fool has positions in and recommends Broadcom, Micron Technology, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool has a disclosure policy.

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.

Making the world smarter, happier, and richer.

© 1995 – 2026 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.

About The Motley Fool

Our Services

Around the Globe

Free Tools

Affiliates & Friends

Micron stock has gained 270% so far this year, propelling the company's market cap above $1 trillion.

Micron Just Crossed $1,000 a Share. Here's the Math on Where It Goes Next. – The Motley Fool

Home

Technology

Micron Just Crossed $1,000 a Share. Here's the Math on Where It Goes Next. – The Motley Fool

Leave a Reply