Shares of Micron Technology (MU +8.80%) have rocketed higher over the past year, jumping by an impressive 831% as of this writing. The chipmaker has been reaping the benefits of the massive surge in memory demand.

Its revenue and earnings have been growing exponentially, powering the stunning rally in Micron stock. However, you may be wondering whether Micron has room to move higher after its astronomical run. After all, the stock's 12-month median price target of $1,100 suggests that it could drop 3% from current levels. But what's worth noting is that 46 of the 49 analysts covering Micron rate it as a buy.

In fact, I won't be surprised to see analysts raising their price targets given the demand-supply conditions in the memory industry. More importantly, the favorable industry factors driving Micron's growth are likely to persist in the long run. That's why it would be a good idea to take a hard look at Micron's prospects over the next five years to understand how profitable a long-term investment in Micron could be.

Image source: Micron Technology.

Micron's dynamic random-access memory (DRAM) and NAND flash storage chips play a mission-critical role in artificial intelligence (AI) data centers. The company is helping hyperscalers scale the memory wall with its high-bandwidth memory (HBM) chips, which are essential for transporting enormous data sets quickly to graphics cards and other AI accelerators.

Memory has emerged as a key bottleneck in the AI infrastructure space. AI accelerators, such as graphics processing units (GPUs) and custom processors, can perform massive amounts of computation quickly, ensuring that AI model training and inference applications run seamlessly. However, they need to be constantly fed with huge amounts of data, and this is what HBM does.

Not surprisingly, memory manufacturers have been producing more HBM, but that isn't proving to be enough as almost all the major companies in this sector have sold out their capacity for 2026. What's more, the HBM market is slated to expand at an annual rate of 30% through the end of the decade, according to industry giant SK Hynix.

This growth is the biggest reason why the memory industry will remain undersupplied over the next five years. Memory manufacturers have been prioritizing the production of HBM and enterprise-grade DRAM over NAND flash memory and conventional DRAM. A Bank of America report released in April noted that HBM consumes three to four times the production capacity required to make conventional memory.

As a result, a structural shortage is emerging in the memory market. Hyperscalers and AI companies are spending hundreds of billions of dollars to build more data centers, and their deep pockets suggest their appetite for HBM won't drop.

Investors should also note that memory manufacturers have an incentive to produce more HBM, as it reportedly generates higher margins than memory modules deployed in consumer electronics such as personal computers (PCs). As a result, there is a shortage of memory chips used in PCs, smartphones, gaming consoles, and automotive applications. These industries are grappling with high memory costs. Hyperscalers and AI companies, however, are unfazed by the cost factor, as they are sitting on backlogs running into more than $2 trillion.

So, it is easy to see why Nvidia CEO Jensen Huang recently pointed out that the ongoing memory shortage will last for "quite a few years," as reported by Reuters. Now that we have seen that Micron's biggest catalyst — low memory supply and the accompanying strength in prices — is sustainable, there is a good chance it will deliver multibagger returns despite having risen remarkably over the past year.

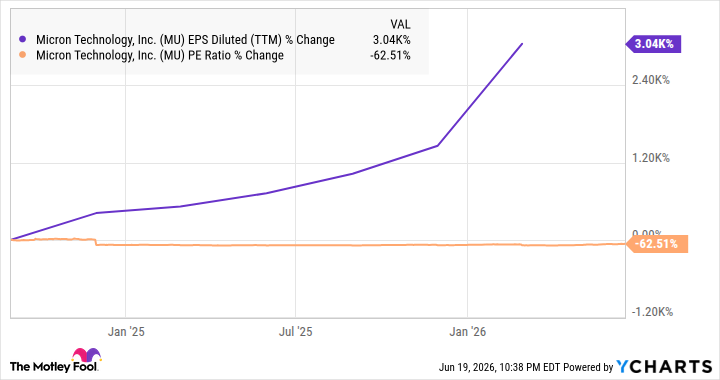

Micron's exponential earnings growth is evident in the following chart, which also shows its price-to-earnings ratio, indicating that its terrific growth potential hasn't been fully priced in yet.

Data by YCharts

While there has been a significant step up in Micron's earnings growth, its earnings multiple has declined. This suggests investors can still buy Micron at an attractive valuation. The stock has a trailing earnings multiple of 53, and its forward earnings multiple of 10.5 points to a huge jump in the bottom line. Consensus estimates are anticipating a 636% increase in Micron's earnings in the current fiscal year 2026 (which ends in August this year) to $61.01 per share.

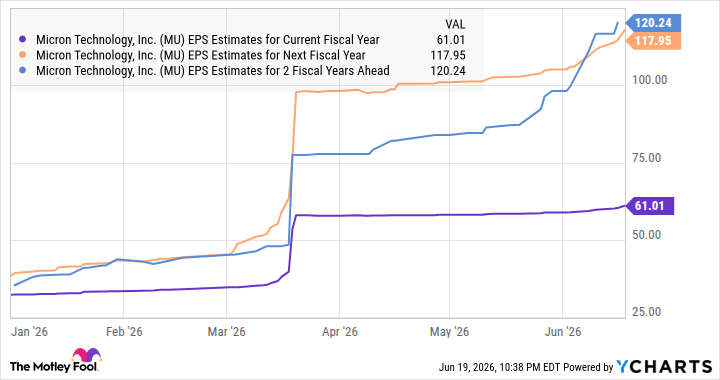

Importantly, analysts are expecting a big jump in Micron's bottom line in the next fiscal year, followed by slightly slower growth in fiscal 2028.

Data by YCharts

However, the chart above clearly shows that the earnings estimate for fiscal 2028 has risen sharply. That's not surprising considering that memory demand is likely to outpace supply for the next five years. Assuming Micron's earnings per share indeed increase to $120.24 in fiscal 2028 (as per the chart above), and it manages to clock even 15% annual earnings growth over the three fiscal years that follow, its bottom line could reach $182.87 per share after five years.

If Micron trades at 26.6 times earnings at that time (in line with the tech-focused Nasdaq-100 index's forward earnings multiple), its stock price could reach $4,864 after five years. That's just over 4x Micron's current stock price, which is why investors looking to add a growth stock to their portfolios can still consider buying it.

Bank of America is an advertising partner of Motley Fool Money. Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Micron Technology. The Motley Fool has a disclosure policy.

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.

Making the world smarter, happier, and richer.

© 1995 – 2026 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.

About The Motley Fool

Our Services

Around the Globe

Free Tools

Affiliates & Friends

A closer look at the memory market's prospects over the next five years suggests that Micron Technology still has multibagger potential.

Leave a Reply