Nvidia is one of the biggest names in the artificial intelligence (AI) infrastructure space since the mainstream adoption of the technology began nearly four years ago, and that's not surprising, as its chips have played an instrumental role in training popular AI models.

However, the AI infrastructure ecosystem has expanded beyond Nvidia. Several companies are witnessing phenomenal growth in their businesses due to significant investments in AI data centers. Applied Digital (APLD +8.62%) is one such company. Its stock has jumped 282% over the past year, well above the 44% jump in Nvidia stock over the same period.

The good news is that it isn't too late to buy Applied Digital stock, as the company has a massive revenue pipeline that keeps getting bigger. Let's see why this AI infrastructure stock has room to run higher.

Image source: Getty Images.

Applied Digital is a pick-and-shovel AI infrastructure company. It designs, builds, and operates dedicated data centers for running AI and high-performance computing (HPC) workloads. The company builds data centers in line with the requirements of hyperscalers and neocloud companies and generates lease revenue by operating those data centers.

Applied Digital recently announced that it has signed a new long-term lease agreement to build an AI factory for a U.S.-based hyperscaler. The company will provide 210 megawatts (MW) of cloud computing capacity to this hyperscaler over 15 years for $5.2 billion. Applied Digital adds that this contract could extend to 30 years, potentially generating $12.7 billion in lifetime lease revenue if its customer exercises all the renewal options.

What's worth noting is that this is the third long-term lease that Applied Digital has entered into with this particular hyperscaler. The AI infrastructure specialist now has contracts to build five AI factory campuses. It expects to generate $36 billion in lifetime lease revenue in a base-case scenario from all of its contracts.

Applied Digital points out that its lease revenue pipeline could jump to $86 billion if all the renewal options are exercised by its existing customers. Not surprisingly, the company's growth is expected to take off, paving the way for more upside.

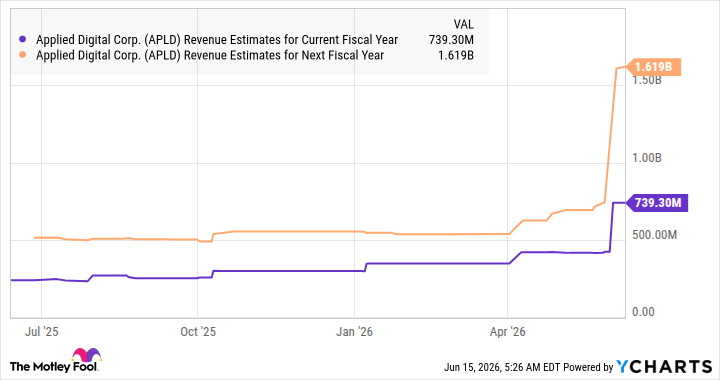

Applied Digital's revenue in the recently concluded fiscal 2026 (which ended last month) is estimated to have jumped by 96% to $422 million. The phenomenal lease pipeline explains why analysts are anticipating a significant acceleration in the company's revenue growth.

Data by YCharts

Applied Digital can sustain such outstanding growth beyond the next couple of fiscal years by building more data centers, which should allow it to convert its lease agreements into revenue. Of course, the stock is expensive at 35 times sales, but it has a strong enough pipeline to justify that multiple.

That's why it isn't too late for investors to buy Applied Digital, as this AI infrastructure play is just getting started.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

*Average returns of all recommendations since inception. Cost basis and return based on previous market day close.

Invest better with The Motley Fool. Get stock recommendations, portfolio guidance, and more from The Motley Fool's premium services.

Making the world smarter, happier, and richer.

© 1995 – 2026 The Motley Fool. All rights reserved.

Market data powered by Xignite and Polygon.io.

About The Motley Fool

Our Services

Around the Globe

Free Tools

Affiliates & Friends

The booming demand for AI data centers is supercharging Applied Digital's growth.

Leave a Reply